Article Content

1 Introduction

In recent years, public governance has become one of the main topics in the international development agenda.Footnote1 However, in spite of significant efforts to procure public governance through the rule of law,Footnote2 there seems to be a mismatch between the expectations from policy prescriptions and real-world outcomes.Footnote3 In this regard, the World Bank asserts—in its 2017 World Development Report: Governance and the Law—that legal improvements to the rule of law have rarely succeed in achieving drastic reductions of corruption.Footnote4 Baez-Camargo and Passas (2017) offer a reasonable explanation: the ineffectiveness of reforms to the rule of law may originates from inconsistencies between the de jure governance and the social norms that guide citizens and bureaucrats; that is to say, from the disregard of systemic effects.

This paper studies, theoretically and empirically, the causal linkage between government expenditure, the rule of law, and corruption. We find that improvements to the rule of law do not necessarily generate lower levels of corruption in all countries because, in the real world, (1) the ceteris paribus condition for other policy issues does not hold (partly because of the trade-offs that emerge when prioritizing policy issues) and (2) co-movements in other topics introduce effects that may oppose the traditional conduits of anti-corruption policies (i.e., inverting the net benefit of misbehaving and curtailing the discretionary use of resources). Moreover, while overall increments in public expenditure tend to generate improvements in the rule of law and a fall in corruption, this relationship can easily become fuzzy if the relative levels of expenditure across multiple policy issues is altered.

We argue that the disappointing performance commonly observed in policies attempting to improve public governance is a consequence of dealing with a complex world, in which unexpected outcomes are the result of systemic considerations that produce non-linearities and a rugged landscape; blurring the mapping between policy packages and outcomes. In particular, the existence of spillover effects between socioeconomic indicators, and the associated policy issues, produce externalities that might distort the incentive structure of public officials in charge of implementing such policies. This, in turn, can create non-anticipated opportunities to divert funds under a setting of imperfect supervision. Accordingly, we introduce a systemic perspective that allows us to move beyond the principal-agent framework and consider the implicit trade-offs in any budgeting exercise that supports a multidimensional policy space.

Through simulations with an agent-based model, we produce country-level estimates for 140 nations during a period of 21 years, while taking into account interactions between numerous indicators. Our computational approach has three key advantages over traditional econometric analyses: (1) it does not require pooling cross-national data, so the model is calibrated for each country individually (i.e., it is consistent with the ‘context matters’ premise by incorporating country-specific characteristics); (2) it provides micro-foundations of a causal process that links expenditure, the rule of law, and corruption (i.e., it is more suitable to deal with problems of endogeneity and revere causation), and (3) it can control for the interactions that take place among a relatively high number of indicators (i.e., it is scalable with respect to the dimensions of the policy space).

The rest of the paper is structured in the following way. Section 2 provides a review of the literature on corruption with an emphasis in econometric studies, and presents some stylized facts that are key to understand why another approach is needed. Section 3 introduces the theoretical model, based on tools of agent-computing, network science, behavioral economics, and political economy games. Section 4 indicates the nature of the data employed for the analysis, how the spillover network is estimated, and how the computational model is calibrated. Section 5 presents empirical findings of the model that are consistent with the stylized facts and the hypothesis outlined in this introduction. Finally, Sect. 6 summarizes the arguments and results of this paper, and provides some additional reflections.

2 On the study of corruption and the rule of law

2.1 The principal-agent view versus a systemic analysis

Broadly speaking, the empirical literature on the determinants of corruption tends to agree on the statistical significance of the rule of law (hereby called the RoL), when tested in a cross-sectional setting. At the same time, however, there is disappointment among international organizations and NGOs with regards to the poor performance of institutional reforms inspired in such literature (World Bank 2017, pp. 77–79). We argue that such discrepancy originates from a view that focuses exclusively on the principal-agent problem (Rose-Ackerman 1975; Klitgaard 1988),Footnote5 and that assumes a ceteris paribus condition. From such perspective, corruption arises from the presence of asymmetric information between the agents (i.e., public servants or elected officials) and a principal (i.e., government or voters) whose monitoring efforts are imperfect. Consequently, improvements to the RoL should reduce the agents’ expected net benefits from embezzling funds and curtail opportunities for the discretionary use of public resources.Footnote6 One of the problems with the principal-agent view is that systemic properties of corruption are considered irrelevant. Thus, the co-evolution of other policy issues is assumed irrelevant in the incentive structure of the agents.

2.2 Econometric studies

The econometric literature on the determinants of corruption is extensive and shows consensus with respect to the statistical significance of the RoL. The theory proposed in this paper aligns with this consensus in several ways, but differs in others. In particular, considering the interactions between different policy issues is not standard in these studies. Furthermore, due to data limitations, country-specific policy prescriptions are difficult to infer through traditional econometric frameworks. In this section, we review some studies and elaborate on ways in which a computational approach could complement them.

Early studies on the determinants of corruption exploit the cross-national variation of different development indicators through pooled-regressions (Ades and Tella 1997; Leite and Weidmann 2002; La Porta et al. 1999; Treisman 2000; Broadman and Recanatini 2001; Dollar et al. 2001; Paldam 2002; Fisman and Gatti 2002; Herzfeld and Weiss 2003; Brunetti and Weder 2003; Knack and Azfar 2003). Overall, these studies have been consistent with the idea that public governance instruments are effective tools that can be used in the fight against corruption. As the econometric literature has progressed, more sophisticated approaches have been deployed in order to overcome some of the limitations in these works and to provide a fine-grained picture of the relevant policy tools.

In studies using Bayesian Model Averaging (BMA),Footnote7 Gnimassoun and Massil (2016) and Jetter and Parmeter (2018) find that some policy variables are robust predictors and, thus, they can be utilized by governments for abating corruption in relatively short periods. Some of these predictors include quality of education, female participation in parliament, willingness to delegate authority, freedom of the press, burden of regulation, absence of political rights, property rights and rule of law (at least in one of the statistical analyses presented in those studies). It is important to emphasize that institutional covariates have a prominent role in this set of explanatory variables.

Jetter and Parmeter (2018) apply a variant of the BMA to consider endogeneity in a large set of independent variables, instrumented through their one-decade lagged values. They find that, out of 32 potential determinants of corruption across 123 countries, 10 are robust. Furthermore, they identify five determinants with direct policy instruments: years of primary education, trade freedom, rule of law, federal system, absence of political rights. Note that the last three are associated to the country’s governance framework. Consistent with most cross-sectional studies, the level of economic development (GDP per capita) is also significant.Footnote8

Using quantile regression in order to deal with parameter heterogeneity, Billger and Goel (2009) identify that improvements in democracy have a negative effect on corruption only among the 50% most-corrupt nations. On the other hand, increments in the government size have negligible effects among the most corrupt countries. In an alternative strategy, Gnimassoun and Massil (2016) and Jetter and Parmeter (2018) split the sample by geographical region and development status, respectively. The latter authors, for example, find that the RoL is prominent among developing countries (i.e., non-members of the OECD), implying that the effectiveness of legal accountability diminishes once the quality of the RoL has reached certain level.Footnote9 In this sub-sample, only two of the 11 robust predictors relate to governance (the RoL and absence of political rights) while two more are associated to some policy instrument (foreign direct investment and government size).

In spite of these commendable efforts, there are still empirical challenges that need to be addressed; some related to the course-grained nature of development-indicator data, and others to methodological issues that are inherent to the econometric study of aggregate relationships. Generally speaking, development indicators do not allow exploiting within-country variation (unless an extremely narrow set of covariates is used). While cross-national variation is, then, the dominant factor, its results have limited policy interpretations since the estimated coefficients correspond to a hypothetical country with the average characteristics of the sample. Another problematic issue comes from the Rodrik critique (Rodrik 2012) which points out that policy indicators are not proper exogenous random variables, but conscious and strategic decisions made by governments in an attempt to obtain specific goals. Thus, the choice of development indicators as explanatory variables might not be appropriate.

Furthermore, an additional methodological limitation comes from the Lucas critique, rejecting the assumption that, under regression analysis, the estimated effects during the sampling period will still be valid in an out-of-sample evaluation.Footnote10 For example, given previous evidence on parameter heterogeneity across income groups, a country’s estimates are likely to shift as its economy develops. Hence, in order to try to overcome some of these challenges, we propose a bottom-up computational approach.

2.3 Stylized facts

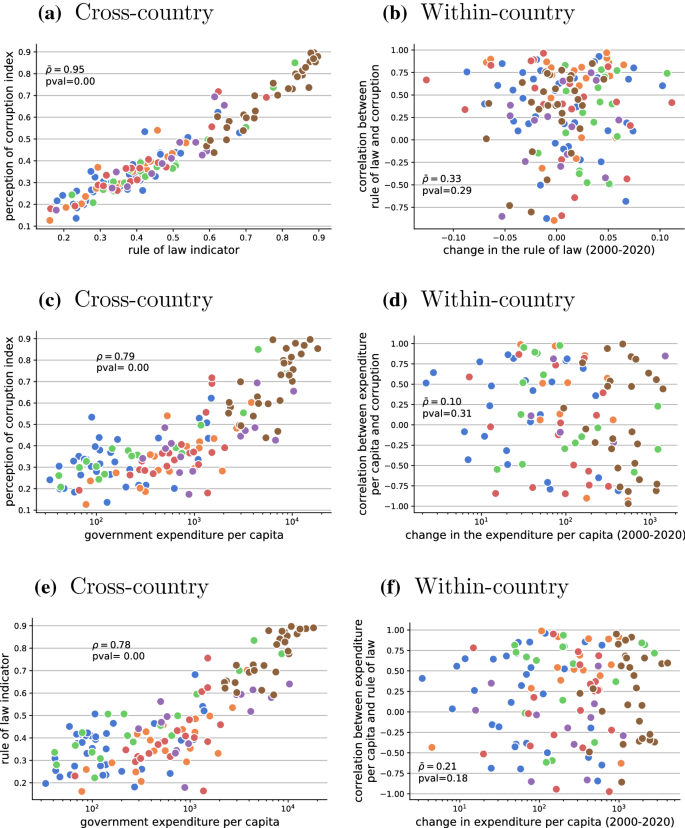

Using an indicator for the RoL—from the 2020 Worldwide Governance Indicators—and the Perception of Corruption Index—from Transparency International—, we corroborate in panels (a) and (b) of Fig. 1 the existence of a paradoxical empirical finding: a high cross-country and a low within-country correlation between corruption and the RoL.Footnote11 The first correlation result is consistent with more sophisticated analyses using cross-section regressions,Footnote12 while the second correlation highlights a missing link between theoretical and empirical studies. Because the vertical axis in panel (b) measures the degree of correlation between corruption (Perception index) and the RoL, this scatter plot indicates that, when analyzing within country variations in the RoL (horizontal axis), there are many countries with a negative relationship between these variables; this stands in contradiction with the policy prescriptions motivated from studies aligned with panel (a).Footnote13 Likewise, in many more cases the positive correlation is relatively low (below 0.33) and, presumably, not statistically significant. Accordingly, all countries (colored dots) with a correlation below the 0.33 threshold are paradoxical cases for the econometric literature supporting improvements in the RoL with the aim of abating corruption.

Source: World Bank’s RoL indicator and Transparency International’s Perception of Corruption Index

Correlations between corruption and intervention variables. Note: Countries are colored by the geographic groups shown in Fig. 2 (color figure online).

In order to propose a potential explanation of these paradoxical results, we also test whether a similar correlation structure exists between the level of per capita government expenditure and each of these two indicators. Panels (c) and (d) present the case for corruption, while panels (e) and (f) do the same but using the indicator for RoL. Because expenditure is a proper instrument of government intervention—as opposed to endogenous development indicators—this paper studies a causal mechanism that goes from expenditure to the RoL and from the RoL to the aggregate diversion of public funds.

Both development indicators are positively correlated with government expenditure per capita in cross-section comparisons. Hence, we hypothesize that, for establishing a conduit between the RoL and corruption, the expenditure channel needs to be studied further. Once more, when within country variations are analyzed, in this case for government expenditure, we find that the correlation between the RoL (or corruption) and per capita expenditure can be either positive or negative. This could be the result of violations to the ceteris paribus assumption and, therefore, it is convenient to analyze such relationships with a framework that incorporates systemic features and the causal mechanisms behind an economy’s emergent properties.

2.4 Proposed methodological framework

In this paper, we take a computational approach and argue that agent-computing can help overcome the problems of reverse causation, non-linearity, parameter homogeneity, and endogenous indicators. To show this, we model an economy’s policymaking process that allows producing country-specific relationships between the RoL and the diversion of public funds. In this model, a government intervention can be established at the level of the overall public expenditure or in the propensity to spend in a specific policy issue.

Micro-founded computational models have the ability of addressing generative causation (Epstein 2006); something that we exploit to produce macroscopic statistical relationships via controlled experiments. Generative causation means that the micro-level social mechanisms from our theory of corruption are formally specified in an algorithm, acting as the data-generating process. Through these experiments, we study the incidence that exogenous government decisions have on the aggregate level of corruption and on the evolution of the RoL. In addition, this approach allows considering the endogenous variation of other policy issues that affect or are affected by the RoL; circumventing the limitations of ceteris paribus assumptions.Footnote14 More specifically, our model highlights three systemic features behind the emergence of corruption that are present in most nations: (1) an adaptive government that establishes budgetary priorities (resource allocations) across several policymaking offices; (2) public servants that make decisions on how to use those resources, and (3) a network of spillovers (externalities) among policy issues (e.g. health, education, infrastructure, public governance, etc.).

2.5 Public expenditure as an exogenous variable

Our empirical strategy consists in generating within-country variation in the level of corruption by exogenously increasing the expenditure dedicated to government programs with the mandate of improving the RoL. By discarding the possibility of intervening the indicator directly, we model a more realistic setting and allow for the endogenous evolution of the RoL, which is not entirely under the control of the central authority (e.g., for example, if the government programs are inherently ineffective).

There are several reasons why expenditure is closer to an exogenous variable in comparison to development indicators, at least in relation to the problem at hand. First, government budgets often come from various processes that are not necessarily related to policy implementation (at least not as strongly as indicators); for example, campaign promises, international agreements, political consensus, societal pressures, political negotiations, or even discretionary decisions. In contrast, empirical development indicators do originate from the policymaking process (which involves inefficiencies such as corruption), thus they are conflated with a wide variety of issues supported by different government programs. Second, when a policy prescription is justified through econometric studies, it is assumed that a change in an indicator equates to a similar change in policy priorities. This is unlikely to be the case since spillover effects and long-term structural factors are partially responsible for the indicators’ dynamics. Thus, changes in expenditure may not necessarily translate into similar changes in the indicators. Third, the opaque mapping between spending and indicators means that more resources to improve the RoL do not necessarily imply less corruption (a common assumption in linear models that use indicators). Thus, using the budget as the exogenous variable allows us to account for potential non-linearities and bottlenecks coming from the data-generating mechanism.

It is important to distinguish between two ways in which an exogenous change in the spending towards the RoL can be implemented. The first type of intervention consists in increasing the total budget available. By doing this, one induces higher success rates in the growth of all indicators because the associated programs are well funded. However, these improvements may be non-linear because the central authority decides how to allocate resources, partially, as a response to observed outcomes (e.g., disparities in the efficient use of resources). Overall, one would expect a negative relation between the size of the budget and the level of corruption if not other policy variable is affected simultaneously. This logic is consistent with cross-national regression studies, since per capita expenditure correlates with how developed is an economy.

The second type of intervention consists of inducing a higher propensity to spend in the RoL while keeping the same budget size. The theoretical implication here is that increments in expenditure towards the RoL take place at the cost of other policy issues. Thus, the relationship between more resources and less corruption is less clear than with the first type of intervention. Naturally, a combination of both types of budgetary changes takes place in the real world. As we argue, below, this may be an important factor to explain the poor experiences of some countries in curbing corruption through reforms to the rule of law.